The IRS has produced up to date recommendations on how to respond to the notorious digital currency issue – “At any time for the duration of 2020, did you get, market, deliver, trade, or in any other case obtain any fiscal interest in virtual forex?” – on 2020 Sort 1040. The updated version as of December 31, 2020, clarifies what’s lined under the phrase, “virtual currency”, and helps make cryptocurrency buys issue to this dilemma.

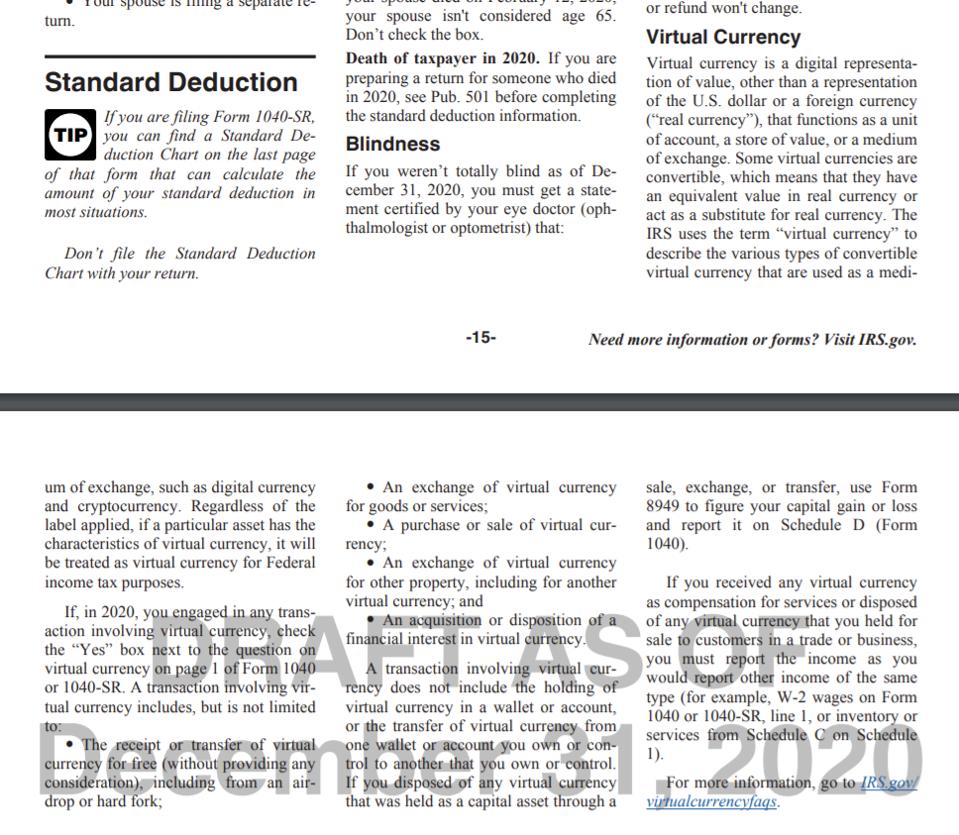

IRS Kind 1040 Directions current as of December 31, 2020

The new draft directions explain how the IRS interprets digital currency.

“The IRS works by using the phrase “virtual currency” to explain the many types of convertible digital forex that are applied as a medium of trade, such as digital forex and cryptocurrency”

The IRS also having a quite broad approach when it will come to what could be addressed as virtual forex for the applications of this concern.

“Regardless of the label utilized, if a individual asset has the features of virtual forex, it will be addressed as virtual currency for Federal cash flow tax purposes”

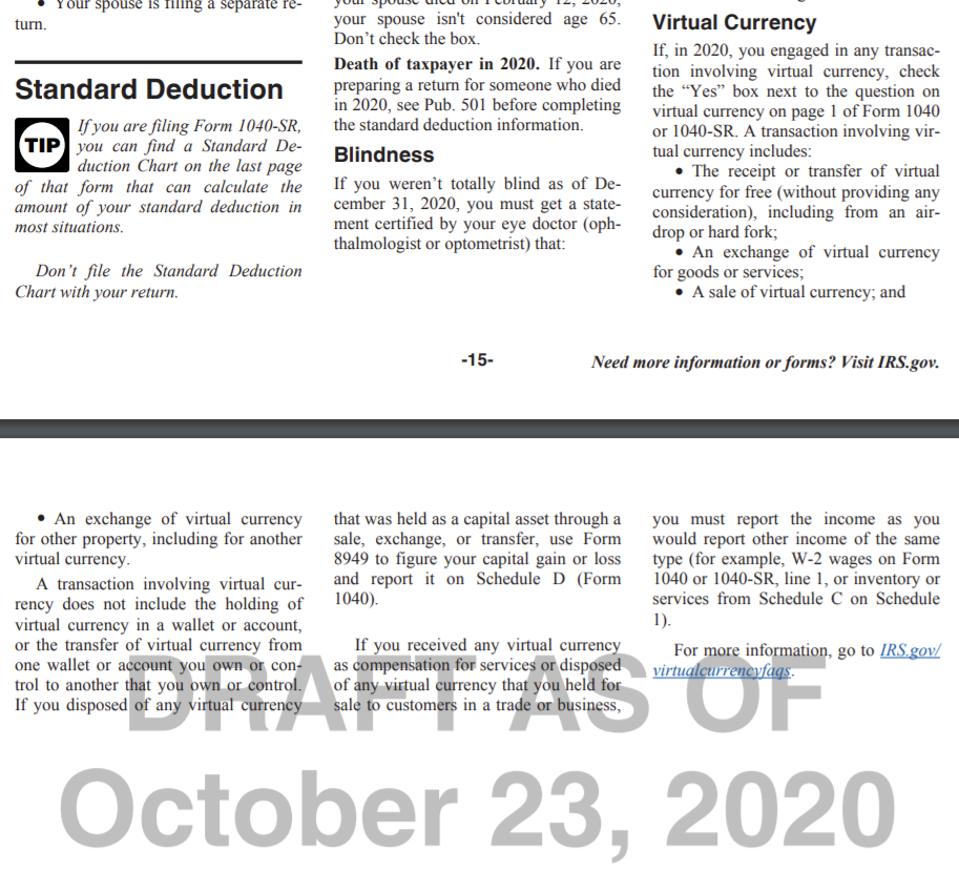

Next, the up to date recommendations clearly state that transactions involving virtual forex include things like buys of virtual forex. This means if you purchased cryptocurrency through 2020, you will have to verify “yes” on the digital currency dilemma on webpage 1 even though this may well not trigger any taxable function. Prior draft recommendations dated Oct 23, 2020 did not explicitly mention this.

IRS Type 1040 Recommendations current as of Oct 23, 2020

Considering that the inclusion of the virtual forex question on 2019 Routine 1, What is particularly lined below this query has been a warm topic in the crypto local community and among the tax practitioners owing to constrained guidelines all-around it. The current recommendations attempt to demystify at the very least some ambiguities.

Disclaimer: This submit is informational only and is not intended as tax tips. For tax suggestions, please seek the advice of a tax experienced.